![Landscaping business loans: What you need to know [2025]](/_next/image?url=https%3A%2F%2Fimages.ctfassets.net%2F3cnw7q4l5405%2F1P8m4go3XWyZVtLcJm0MUg%2F603727aaa2fe5e0738fa3f64cd90f2a1%2FLandscaping_business_loans__What_you_need_to_know_-2025-.png&w=3840&q=75)

Table of Contents

Table of Contents

- What is a landscaping business loan?

- What are the different types of landscaping business loans?

- 1. Term loans

- 2. SBA loans

- 3. Equipment financing

- 4. Business lines of credit

- 5. Invoice financing

- What are the requirements to qualify for a landscaping business loan?

- How to apply for landscaping business loans?

- How to use a landscaping business loan?

- It’s your turn now

- Frequently Asked Questions (FAQs)

- What is the best loan for landscapers?

- What credit score is needed for a landscaping business loan?

- How much can you borrow with a landscaping business loan?

- What are the interest rates for landscaping business loans?

- How long does it take to get approved for a landscaping business loan?

- How to apply for landscaping business loans?

- How to use a landscaping business loan?

- It’s your turn now

- Frequently Asked Questions (FAQs)

- What is the best loan for landscapers?

- What credit score is needed for a landscaping business loan?

- How much can you borrow with a landscaping business loan?

- What are the interest rates for landscaping business loans?

- How long does it take to get approved for a landscaping business loan?

Ever heard the phrase, you need money to make money?

That saying couldn’t be more true for landscaping businesses.

Access to funds is essential, whether it’s to start, grow, or sustain the company during the slow winter season. It can help you purchase new equipment, hire employees, or smooth out cash flow.

But where do you find such financing?

One option worth exploring is a business loan.

In this guide, you’ll learn all you need to know about landscaping business loans, including:

The requirements needed to qualify for business loans.

The best financing solutions to support business growth.

How to apply for financing opportunities.

What is a landscaping business loan?

A landscaping loan gives your business the funds needed to cover expenses.

It can be used for various purposes such as:

Purchasing new equipment.

Covering an unexpected shortage in cash flow.

Expanding services.

Hiring or paying staff.

Starting or growing a landscaping business.

Promoting your services to acquire new customers.

Landscaping businesses can secure loans from various lenders, such as the government, banks, credit unions, or online lenders. Each offers different types of loans with unique eligibility requirements and conditions.

What are the different types of landscaping business loans?

Whether purchasing equipment, fueling your vehicles, or paying salaries, here are the top loan options for financing your landscaping business.

1. Term loans

This financing option gives landscaping businesses access to a large sum of money at a fixed or variable interest rate. It’s best suited for companies with clear financial records and typically offers flexible repayment options— monthly, quarterly, or annually—over 1 to 20 years. According to LendingTree, average interest rates for term loans are 7.38% for fixed rates and 7.84% for variable rates.

Once approved, borrowers receive a lump sum and repay it over a period. Term loans can be used to:

Purchase new equipment to maintain or grow a landscaping operation.

Expand inventory, e.g., stocking up on fertilizers, seeds, plants, and essential items.

Cover operating expenses such as rent, utilities, and payroll to keep the landscaping business running.

Expand the business or renovate existing structures.

Market your services to secure new customers during peak seasons: truck branding, digital promotional campaigns, or personalized materials to prospect mailboxes.

Hire and train additional employees.

Pros:

Access to large sums of cash at once ($5,000 to $5 million, depending on the financial institution).

Offers short and long-term repayment plans based on your current needs.

Direct approval path, especially if your finances are in order.

Cons:

Requires detailed financial records and strong credit scores.

Needs collateral, or you risk losing assets if you default.

The total lending cost can be high, especially with longer repayment terms.

2. SBA loans

An SBA loan is a type of loan guaranteed by the U.S. Small Business Administration. Now, the SBA doesn’t lend directly—instead, it partners with banks and other financial institutions to provide money to business owners.

Through this partnership, landscaping companies can access various loan programs, such as SBA 7(a), SBA microloans, and 504 loans.

The 7(a) (which is up to $5 million) is the SBA’s primary loan program, and it allows you to:

Purchase equipment

Refinance existing debt

Start or buy out a landscaping business

Get cash for the business’s daily expenses

It offers multiple interest rates depending on the loan amount. Loans between $50k and $350k attract a 4.5% to 6.5% interest rate, while amounts above $350k do not exceed 3%.

There’s also the microloan program for small businesses building their credit. It offers up to $50,000 and can be used to start, grow, or sustain the landscaping business.

Lastly, you have 504 loans offering fixed-rate financing (3% of the debt) for fixed assets, such as the purchase of real estate, office construction, or fixed equipment. However, it can’t be used for working capital or leasing equipment.

Pros:

Offers financing of up to $5 million.

SBA 7(a) loans can be used to refinance an existing debt.

Maximum loan maturity is up to 5 years.

Cons:

SBA 7(a) loans have lengthy approval times.

7(a) and 504 loans require high credit scores (680+) for approval.

Depending on the loan program, a down payment may be required (e.g., 504).

3. Equipment financing

This loan option allows you to upgrade or purchase new equipment, such as a leaf blower, trailer, equipment shed, or even shears. You can secure between $25k and $100k+ loan funding from financial institutions with interest rates between 5.99% and 7%.

Here, you get a quote from the vendor and take it to lenders for financing.

The good thing about equipment financing is that it’s self-collateralized, which means the tool becomes the collateral if you default on payment.

Pros:

Some lenders don’t have any time-in-business requirement, allowing startups to apply for financing.

Typically offers fixed interest rates since equipment loans are secured.

Fast approval times.

Cons:

May require a large down payment.

The tool might become obsolete while you’re still making payments.

Certain lenders require additional collateral to approve funding.

4. Business lines of credit

This option gives you access to a certain amount that you can withdraw. You only pay interest on the money used, not the total credit limit.

It’s excellent for covering emergencies, funding small projects, working cash, or managing seasonal cash flow gaps.

And once you pay back the borrowed amount, your full credit limit becomes available. In other words, you borrow, repay, and borrow again without reapplying.

Pros:

Provides reusable funds and allows you to borrow only what you need.

It has a simple approval process with some lenders offering same-day access to funds.

Quick access to working capital.

Cons:

Might take on more debt than necessary, which can lead to a cycle of debt.

Requires your landscaping business to have been operational for at least six months.

Some lenders charge a fee on every withdrawal from your credit line.

5. Invoice financing

Use unpaid invoices as collateral to get funds for your landscaping business. Lenders will provide you with about 100% funding of the total invoice value.

When clients pay, the lender recoups their money and pays the remaining balance to you.

This loan option provides your landscaping business with steady cash, all the money it needs to run.

Pros:

No personal credit is required for invoice financing as it’s based on the credit history of the invoiced business.

Receivable accounts are the loan collateral, so no additional guarantees are required.

Quick access to working capital for new landscaping companies.

Cons:

The amount available depends on outstanding invoices, which makes it an unreliable funding source.

Your business should be making $10k per month in a business bank account.

It could negatively impact a client’s perception of your business if they are forced to deal with third parties.

What are the requirements to qualify for a landscaping business loan?

First, understand that different lenders have unique requirements for evaluating loan applications.

But in general, here are the requirements most financial institutions need:

Credit score: Most lenders require a credit score of 600+. However, a high credit score improves your chances of approval. To get SBA 7(a) loans, for instance, you’ll need a credit score of 680+.

Time in business: While financing opportunities exist for new landscaping businesses, certain lenders require at least six months of operating history to qualify for a loan.

Annual revenue: Stable revenue is a crucial factor in loan applications. Many programs, such as SBA 504, invoice financing, equipment financing, term loans, and business lines of credit, expect companies to generate at least $10k monthly in revenue.

Collateral: You might need additional collateral for specific loan programs, such as SBA 7(a) or unsecured lines of credit. The collateral can be real estate, fixed equipment, receivable accounts, or personal assets.

To ensure a smooth process during your application, prepare a solid business plan with clear documentation of current assets and liabilities to show lenders you have what it takes to repay the loan.

You also need an updated record of your financial statements. Do you know what your average landscaping project costs? What’s the profit on each job? How about profit and loss margin?

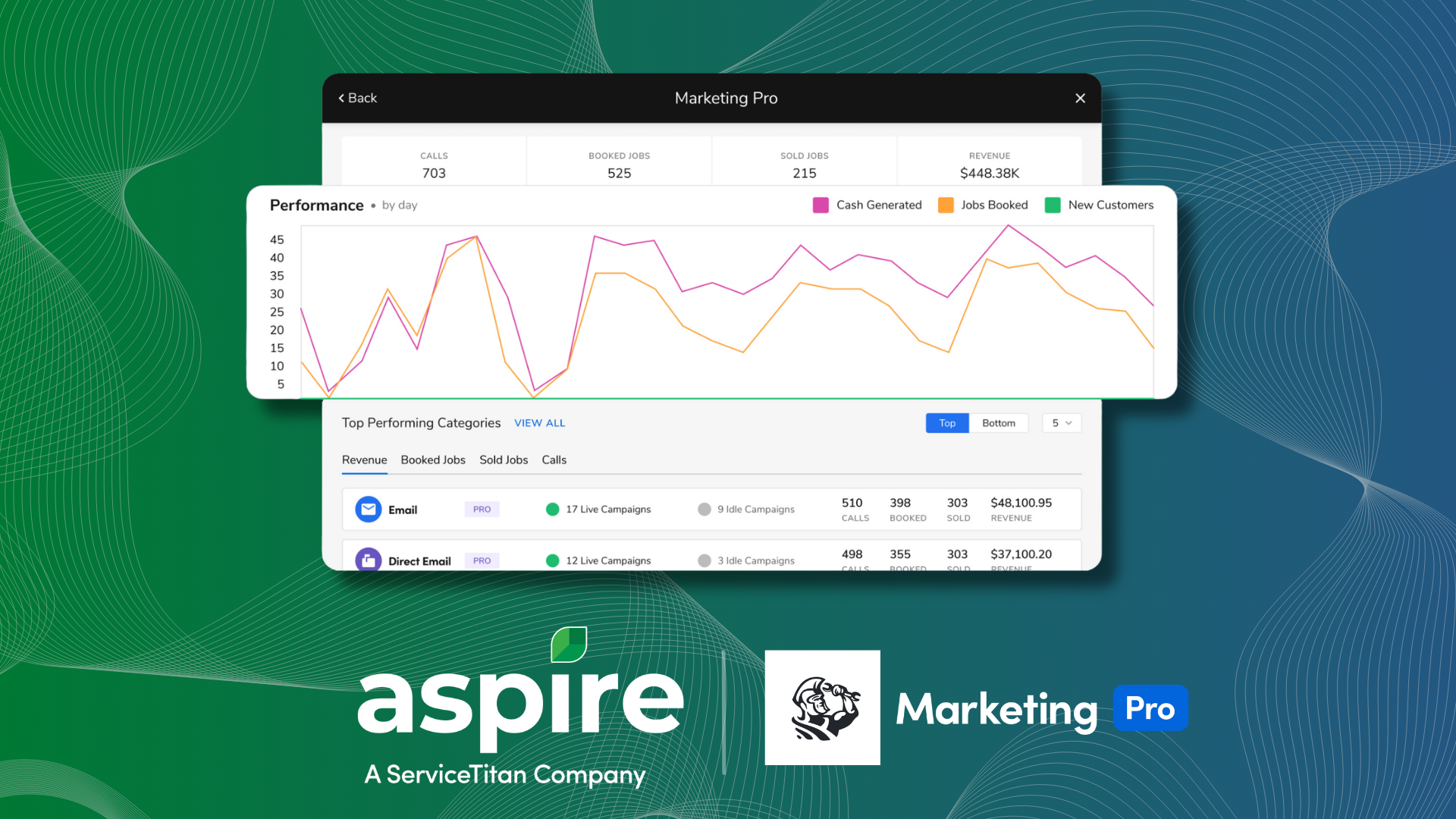

Don’t know how to get such accurate financial data?

Aspire’s financial reporting allows you to improve your financial tracking and showcase strong documentation to lenders.

![Landscaping business loans: What you need to know [2025] > Screenshot 1](https://images.ctfassets.net/3cnw7q4l5405/1IixSnQsftXltdxDhr4mBr/cb967731393cfcaa55fdfb53ab20e779/Aspire_profit_and_loss_margin.png)

It enables you to monitor business revenue, gross profit, and loss. Whether you want a general or a specialized report showing labor, equipment, or material costs, Aspire helps centralize your data.

This ensures you have all the financial information you need to make strategic financial decisions or present to institutions to receive funding.

How to apply for landscaping business loans?

Landscaping businesses are seasonal and often face cash flow shortages, so your loan application process needs extra effort.

For instance, you may need to explain how you’ll use the funds and your repayment plan with a clear budget.

To simplify the process, here’s a checklist to follow.

Determine how much you need and what the money will be used for, e.g., equipment purchase, starting or buying a landscaping business, or working capital.

Choose the loan type that best suits your needs—SBA 7(a) or 504, term loans, equipment financing, or line of credit.

Find and compare lenders carefully. Before committing, look at interest rates, additional fees, repayment terms, and approval timelines to find the best fit.

Once you find a lender, confirm the eligibility requirements. Do you have the needed credit score, annual revenue, collateral, or time in business?

Prepare your documents: financial reports, credit reports, tax returns, business structure and plan, cash flow forecast, personal ID, legal documents, and business licences.

Submit your application online or in person, depending on the lender.

How to use a landscaping business loan?

Want to hire seasonal staff and expand your business? A loan program like SBA 7(a) could be perfect for you.

Refinancing an existing debt? Both the 7(a) and 504 are great choices.

The point is, there are several ways to use a landscaping business loan. Here are some of the major ones:

Purchasing equipment and vehicles: From heavy-duty trucks to computers for smooth operations, professional mowers, or trimmers, you can use a landscaping equipment loan to secure new tools for your business. It can also fund new landscaping management software like Aspire to help schedule, report, estimate, and manage client relationships.

Increasing marketing efforts: Use the loan funding to promote your services to new customers or cross-sell opportunities like hardscaping or construction space heaters to existing customers.

Hiring staff and covering payroll: It’s the busy season. Projects are piling up, and you have limited manpower to handle available jobs. You can use loans to hire and pay new staff before the invoice clears.

Managing seasonal cash flow gaps: You never have to be strapped for cash or wonder where to get money to keep the business afloat during slow seasons. Loans like SBA 7(a) or invoicing financing can be used to manage cash flow gaps.

Expanding your landscaping business: Starting a new location for your business can be expensive. You’d have to rent an office, get new equipment, hire staff, and pay bills. Instead of saving funds to start from scratch, you can leverage business loans to get started.

It’s your turn now

You’ve seen how to secure funding and keep your landscaping business running through those slow winter seasons.

Now, it’s time to find the best loan option to support your growth all year round.

A tool like Aspire makes the loan application process easier by helping collect all the necessary documents through intelligent reporting.

Instead of wading through several files to find documents, Aspire centralizes all your operations, giving you fast access to critical financial data, like annual revenue, active projects, cash flow, and profit and loss margin on each job.

By using Aspire, you can better understand your landscaping business’s financial health, which could improve your chances of being approved by lenders.

Book a demo with Aspire today and see how it can help keep your financial data in order.

Frequently Asked Questions (FAQs)

What is the best loan for landscapers?

The best loan depends on different factors such as your current needs, revenue, and financial history.

But you can classify them based on approval time.

For quick-approval loans, lending programs such as invoice financing or lines of credit provide quick access to cash. This ensures you have cash flow to cover working expenses and fuel your business growth.

What credit score is needed for a landscaping business loan?

The ideal credit score needed for landscaping business loans ranges between 550+ and 600.

How much can you borrow with a landscaping business loan?

Based on data from various financial institutions, landscaping business loans typically range from $50k to $5.5 million, depending on your business qualifications and the lender.

What are the interest rates for landscaping business loans?

Interest rates typically range between 6% and 15% based on your preferred loan program.

SBA loans: 5%-13%

Equipment financing: 5.99% to 7%

Term loans: 7.38% for fixed rates and 7.84% for variable rates.

Business lines of credit: 6%+

Invoice financing: 2%+

How long does it take to get approved for a landscaping business loan?

Depending on the lender, it can take anywhere from a few hours to months.

Equipment financing: 24-72 hours

Term loans: 24 hours to 3 months

Business lines of credit: 28-48 hours

SBA loans: Three weeks

Invoice financing: 24-72 hours